Dear readers welcome, today in this article we provide the information related to Journal Entries with examples. After reading the article you will get the knowledge to pass the basic journal entries. These Journal Entries are very important in Accounting.

Lets start one by one

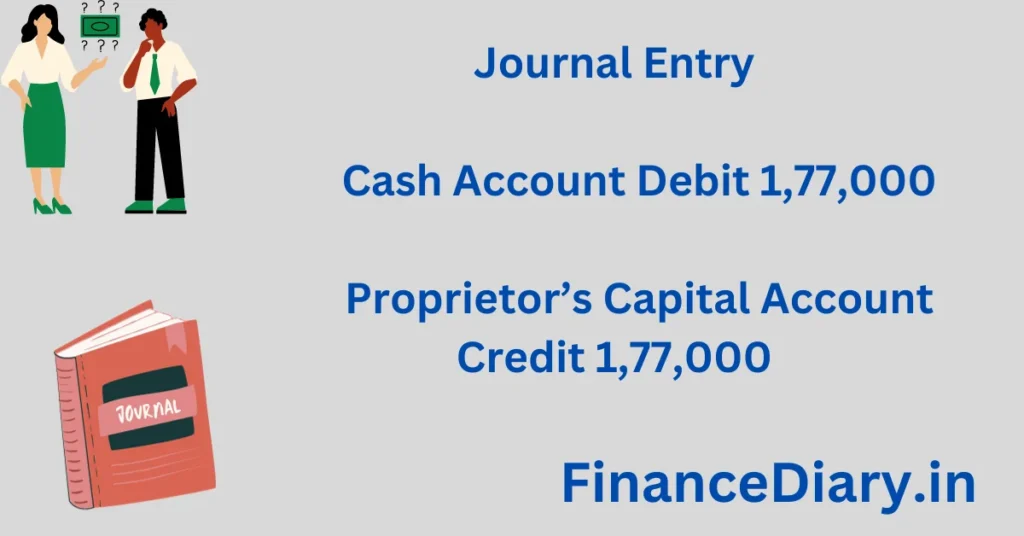

CASH BROUGHT IN BY PROPRIETOR AS CAPITAL RS. 1,77,000

Journal Entry:

Cash Account Debit 1,77,000

Proprietor’s Capital Account Credit 1,77,000

Explanation:

In this transaction, the proprietor (the owner of the business) brings in cash as capital to invest in the business.

Cash Account Debit: The cash account is debited because cash is an asset, and when it increases, we debit it to show that it’s coming into the business.

Proprietor’s Capital Account Credit: The proprietor’s capital account is credited because capital represents the owner’s equity in the business. When the owner invests more capital, it increases the equity, and we credit the capital account to reflect this increase.

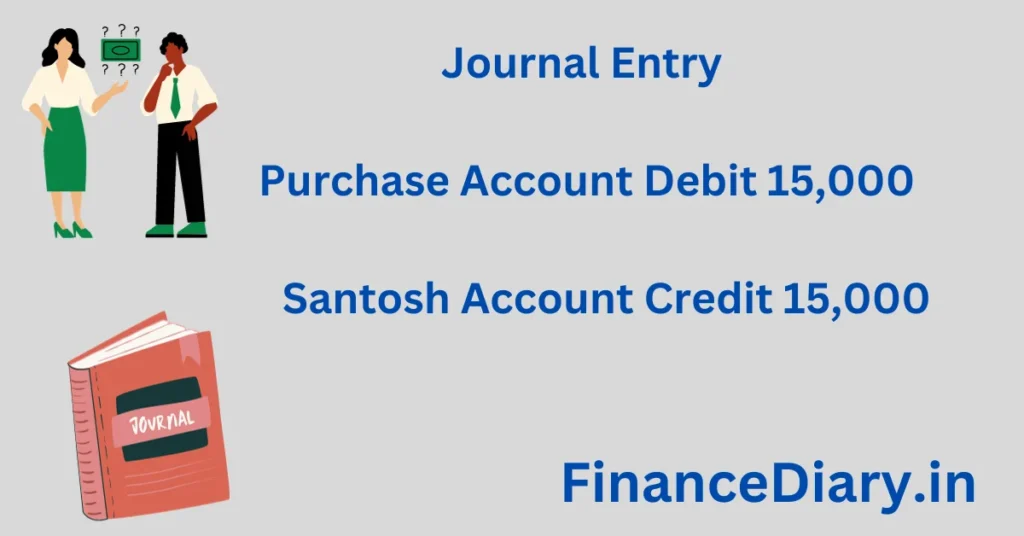

GOODS PURCHASED ON CREDIT FROM SANTOSH RS. 15,000

Journal Entry:

Purchase Account Debit 15,000

Santosh Account Credit 15,000

Explanation:

In this case, the business purchases goods on credit from Santosh, a creditor.

Purchase Account Debit: The purchase account is debited because goods are coming into the business, and we debit expenses or asset accounts when they increase.

Santosh Account Credit: Santosh account is credited because he is the creditor from whom the goods were purchased on credit. We credit the account of the person or entity we owe.

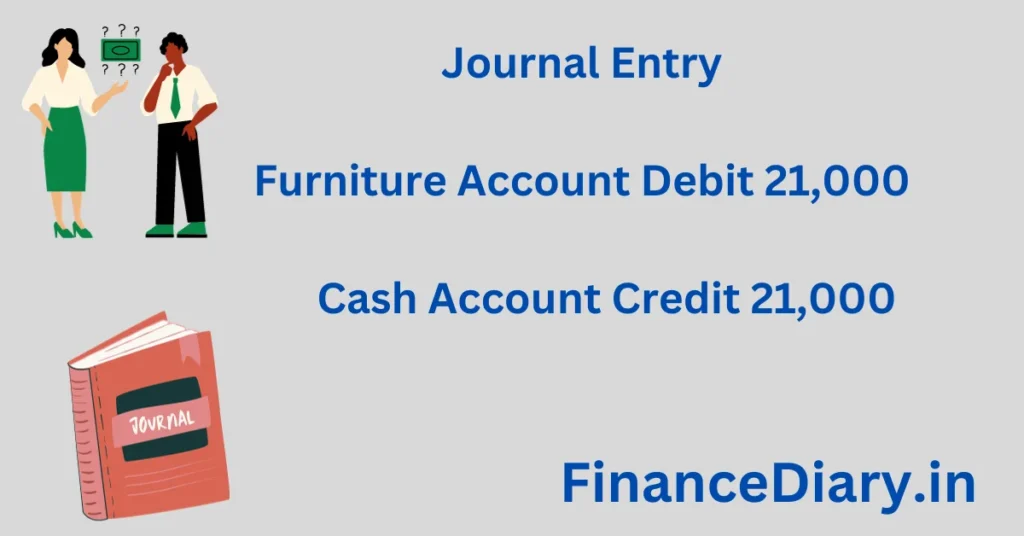

FURNITURE PURCHASED FOR CASH RS. 21,000

Journal Entry:

Furniture Account Debit 21,000

Cash Account Credit 21,000

Explanation:

In this transaction, the business buys furniture and pays for it in cash.

Furniture Account Debit: Furniture is an asset, and when it’s acquired, we debit the furniture account to increase the asset.

Cash Account Credit: Cash is decreasing because it’s being used to pay for the furniture, so we credit the cash account.

GOODS SOLD ON CREDIT TO DEV RAJ RS. 11,600

Journal Entry:

Dev Raj Account Debit 11,600

Sale Account Credit 11,600

Explanation:

The business sells goods on credit to Dev Raj.

Dev Raj Account Debit: Dev Raj’s account is debited because he is the receiver of the goods on credit. We debit the personal account of the person who owes us money.

Sale Account Credit: The sale account is credited because sales represent revenue for the business. We credit revenue accounts when they increase.

GOODS PURCHASED FOR CASH RS. 14,500

Journal Entry:

Purchase Account Debit 14,500

Cash Account Credit 14,500

Explanation:

The business purchases goods and pays for them in cash.

Purchase Account Debit: The purchase account is debited because goods are coming into the business, and we debit expenses or asset accounts when they increase.

Cash Account Credit: Cash is decreasing because it’s used to pay for the goods, so we credit the cash account.

Let’s continue with the explanations for the remaining transactions:

GOODS SOLD FOR CASH RS. 22,100

Journal Entry:

Cash Account Debit 22,100

Sale Account Credit 22,100

Explanation:

a) Cash Account Debit: We debit the cash account because cash is coming into the business. When cash increases, we debit it.

b) Sale Account Credit: The sale account is credited because goods were sold, and this represents revenue. We credit revenue accounts when they increase.

RENT PAID FOR SHOP TO LANDLORD RS. 13,000

Journal Entry:

Rent Account Debit 13,000

Cash Account Credit 13,000

Explanation:

a) Rent Account Debit: Rent is an expense, and expenses are debited when they increase. In this case, the business is incurring rent expenses.

b) Cash Account Credit: Cash is an asset, and it’s decreasing as it’s being paid to the landlord. Assets are credited when they decrease.

COMMISSION RECEIVED IN CASH RS. 22,000

Journal Entry:

Cash Account Debit 22,000

Commission Account Credit 22,000

Explanation:

a) Cash Account Debit: Cash is debited because it’s coming into the business. Cash increases, so we debit it.

b) Commission Account Credit: Commission received is income for the business, and income accounts are credited when they increase.

CASH DEPOSITED INTO BANK RS. 25,000

Journal Entry:

Bank Account Debit 25,000

Cash Account Credit 25,000

Explanation:

a) Bank Account Debit: The bank account is debited because cash is being deposited into the bank. Assets (bank balance) increase when debited.

b) Cash Account Credit: Cash is credited because it’s decreasing when being moved from the cash on hand to the bank.

CASH WITHDRAWN FROM BANK FOR OFFICE USE RS. 12,000

Journal Entry:

Cash Account Debit 12,000

Bank Account Credit 12,000

Explanation:

a) Cash Account Debit: Cash is debited because it’s coming into the business from the bank. Cash increases when debited.

b) Bank Account Credit: The bank account is credited because cash is being withdrawn from the bank. Assets (bank balance) decrease when credited.

CASH DRAWN BY PROPRIETOR FROM BUSINESS FOR PERSONAL USE RS. 43,000

Journal Entry:

Drawing Account Debit 43,000

Cash Account Credit 43,000

Explanation:

a) Drawing Account Debit: The drawing account is debited because the proprietor is withdrawing cash for personal use. This withdrawal reduces the proprietor’s capital in the business.

b) Cash Account Credit: Cash is credited because it’s decreasing as the proprietor is taking it out for personal use.

GOODS GIVEN AS CHARITY RS. 11,000

Journal Entry:

Charity Account Debit 11,000

Purchase Account Credit 11,000

Explanation:

a) Charity Account Debit: Charity is considered an expense of the business, so it’s debited as it increases expenses.

b) Purchase Account Credit: Goods given as charity reduce the inventory (goods) of the business, so the purchase account is credited to reflect this decrease.

BAD DEBTS WRITTEN OFF RS. 1500 JOURNAL ENTRIES WITH EXAMPLES

Journal Entry:

Bad Debt Account Debit 1500

Debtor Account Credit 1500

Explanation:

a) Bad Debt Account Debit: Bad debt represents a loss for the business as a debtor fails to pay, so it’s debited.

b) Debtor Account Credit: The debtor’s account is credited because the debtor is no longer expected to pay, which reduces the asset of accounts receivable.

BAD DEBTS RECOVERED IN CASH RS. 2300

Journal Entry:

Cash Account Debit 2300

Bad Debts Recovered Account Credit 2300

Explanation:

a) Cash Account Debit: Cash is debited because it’s coming into the business as a recovery of previously written off bad debts.

b) Bad Debts Recovered Account Credit: Bad debts recovered represent income for the business, so it’s credited when it’s received.

CARRIAGE PAID ON MACHINERY (EXPENSES ON PURCHASE OF ASSET) RS. 11,000

Journal Entry:

Machinery Account Debit 11,000

Cash Account Credit 11,000

Explanation:

a) Machinery Account Debit: Carriage paid on machinery is considered part of the cost of the machinery, so it’s debited to increase the asset value of machinery.

b) Cash Account Credit: Cash is credited because it’s decreasing as it’s used to pay for the carriage expense related to the machinery purchase.

Certainly, let’s go through the explanations for these additional transactions:

DEPRECIATION ON FIXED ASSETS RS. 2500

Journal Entry:

Depreciation Account Debit 2500

Fixed Asset Account Credit 2500

Explanation:

a) Depreciation Account Debit: Depreciation on fixed assets represents a loss for the business as assets wear out over time, so it’s debited as an expense.

b) Fixed Asset Account Credit: Fixed assets are decreasing in value due to depreciation, so we credit the fixed asset account to reflect this decrease.

CARRIAGE PAID ON BEHALF OF THE BUYER RS. 11,000

Journal Entry:

Debtor Account Debit 11,000

Cash Account Credit 11,000

Explanation:

a) Debtor Account Debit: Carriage paid on behalf of the buyer increases the amount the debtor owes the business. When a debtor owes more, their account is debited to reflect the increase in accounts receivable.

b) Cash Account Credit: Cash is credited because it’s going out to pay for the carriage on behalf of the buyer.

GOODS GIVEN AS FREE SAMPLES RS. 21,500

Journal Entry:

Advertising Account Debit 21,500

Purchase Account Credit 21,500

Explanation:

a) Advertising Account Debit: Goods given as free samples are considered an advertising expense because they are used for promotional purposes. Expenses are debited when they increase.

b) Purchase Account Credit: Goods given as free samples reduce inventory (goods) and are credited to reflect the decrease in the purchase account.

INTEREST ALLOWED ON CAPITAL RS. 1600

Journal Entry:

Interest on Capital Account Debit 1600

Capital Account Credit 1600

Explanation:

a) Interest on Capital Account Debit: Interest allowed on capital is an expense for the business, so it’s debited.

b) Capital Account Credit: Capital is a liability account, and when it increases due to interest being added, it’s credited to reflect the increase in the capital amount.

INTEREST CHARGED ON DRAWINGS RS. 500

Journal Entry:

Drawing Account Debit 500

Interest on Drawing Account Credit 500

Explanation:

a) Drawing Account Debit: Interest charged on drawings represents a decrease in capital (or an increase in drawings), so it’s debited.

b) Interest on Drawing Account Credit: Interest on drawings is treated as income for the business, so it’s credited to reflect the income earned.

BANK CHARGES OR INTEREST CHARGED BY BANK RS. 200

Journal Entry:

Bank Charges Account Debit 200

Bank Account Credit 200

Explanation:

a) Bank Charges Account Debit: Bank charges are considered expenses for the business, so they are debited as they increase expenses.

b) Bank Account Credit: The bank account is credited because it’s decreasing as the bank charges are paid.

GOODS LOST BY FIRE RS. 2800

Journal Entry:

Loss by Fire Account Debit 2800

Purchase Account Credit 2800

Explanation:

- a) Loss by Fire Account Debit: Goods lost by fire represent a loss for the business, so it’s debited as a loss account.

- b) Purchase Account Credit: The purchase account is credited to reduce the value of stock at cost because the goods have been lost.

GOODS INSURED AND A CLAIM IS ADMITTED BY INSURANCE COMPANY IN FULL OR IN PART.

Journal Entry:

Insurance Company Account Debit (Amount as per claim)

Loss by Fire Account Credit (Amount as per claim)

Explanation:

a) Insurance Company Account Debit: The insurance company becomes a debtor because they owe the business money as part of the insurance claim. Debtor accounts are debited when they increase.

b) Loss by Fire Account Credit: The loss by fire account is credited to reduce the loss amount due to the insurance claim.

LOAN TAKEN RS. 2,00,000

Journal Entry:

Cash Account Debit 2,00,000

Lender’s Loan Account Credit 2,00,000

Explanation:

a) Cash Account Debit: Cash is debited because it’s coming into the business as a loan.

b) Lender’s Loan Account Credit: The lender’s loan account is credited because it represents the liability of the business. When a loan is taken, it increases the liability, and we credit the loan account.

INTEREST PAID ON LOAN RS. 1,000

Journal Entry:

Interest on Loan Account Debit 1,000

Cash Account Credit 1,000

Explanation:

a) Interest on Loan Account Debit: Interest paid on a loan is considered an expense for the business, so it’s debited.

b) Cash Account Credit: Cash is credited because it’s decreasing as it’s used to pay the interest expense.

INTEREST ON LOAN DUE BUT NOT PAID IN CASH. RS. 500

Journal Entry:

Interest on Loan Account Debit 500

Loan or Creditor Account Credit 500

Explanation:

a) Interest on Loan Account Debit: Interest on the loan is an expense for the business, so it’s debited.

b) Loan or Creditor Account Credit: This entry reflects that the interest is due but hasn’t been paid in cash yet, so it increases the liability (creditor), and we credit the loan or creditor account.

RELATED ARTICLES

JOURNAL ENTRIES FOR ACCOUNTS PAYABLE

JOURNAL ENTRIES FOR ACCOUNTS RECEIVABLES

JOURNAL ENTRY FOR CHEQUE DEPOSIT IN BANK

JOURNAL ENTRY FOR DISCOUNT RECEIVED

JOURNAL ENTRY FOR CAPITAL INTRODUCED

INVESTMENT PURCHASED RS. 50,000

Journal Entry:

Investment Account Debit 50,000

Cash Account Credit 50,000

Explanation:

a) Investment Account Debit: Investments are assets, and when they are acquired, we debit the investment account to increase the asset.

b) Cash Account Credit: Cash is credited because it’s decreasing as it’s used to purchase the investment.

CASH STOLEN FROM THE OFFICE RS. 6,000

Journal Entry:

Loss by Theft Account Debit 6,000

Cash Account Credit 6,000

Explanation:

a) Loss by Theft Account Debit: Cash stolen from the office is considered a loss for the business, so it’s debited as a loss account.

b) Cash Account Credit: Cash is credited because it’s decreasing due to the theft.

CASH PAID TO A CREDITOR IN FULL SETTLEMENT

(When cash discount is received). Amount due to Madan Lal ₹ 5,000 paid him Rs 4,950 in full settlement.

Journal Entry:

Madan Lal Account Debit 5,000

Cash Account Credit 4,950

Discount Received Account Credit 50

Explanation:

a) Madan Lal Account Debit: The amount due to Madan Lal is debited because it’s decreasing as he is paid in full settlement.

b) Cash Account Credit: Cash is credited because it’s decreasing as it’s paid to Madan Lal.

c) Discount Received Account Credit: A cash discount is received, which is treated as income for the business, so it’s credited.

CASH RECEIVED FROM A DEBTOR IN FULL SETTLEMENT

(When cash discount is allowed). Amount receivable from Dev Raj Rs. 1,600, received from him Rs. 1,570.

Journal Entry:

Cash Account Debit 1,570

Discount Allowed Account Debit 30

Dev Raj Account Credit 1,600

Explanation:

a) Cash Account Debit: Cash is debited because it’s increasing as it’s received from Dev Raj.

b) Discount Allowed Account Debit: A cash discount is allowed, which represents a loss for the business, so it’s debited.

c) Dev Raj Account Credit: The amount due from Dev Raj is credited because it’s decreasing as he pays in full settlement.

These explanations help understand how each of these transactions is recorded in the double entry accounting system, maintaining accurate financial records.

Video Credit : Rajat Arora

CONCLUSION

In this article we provided basic journal entries with examples. If you want to know more kindly comment below. We will update it.