Are you looking to know about CASA full form in Banking? If yes then you came to right blog article.

In this article you get to know about CASA full form in Banking. This article is written after referring and reading more than 21 articles related to CASA.

UNVEILING CASA: UNDERSTANDING ITS IMPORTANCE

In the world of banking, we may often come across the term “CASA,” which full form refers to CURRENT ACCOUNT AND SAVINGS ACCOUNT. CASA plays a important role in the banking sector, as it forms the foundation of a bank’s deposit base. In this article, we will provide detailed information related to the CASA full form in banking, understand its significance, and explore the features and benefits of both current and savings accounts.

CURRENT ACCOUNT

A current account is primarily used by businesses, companies, and enterprises. It is designed to facilitate frequent and large transactions. With a current account, there are no restrictions on the number and amount of transactions that can be made. This flexibility makes it suitable for businesses that need to make numerous payments to suppliers, employees, and other stakeholders.

Current accounts offer various services such as overdraft facilities, cheque books, and online banking, which enable businesses to effectively manage their finances. The availability of an overdraft facility allows businesses to withdraw more money than what is available in their account, up to a certain limit. This feature is crucial for managing cash flow and handling unexpected expenses. Moreover, current accounts provide detailed statements and reports, empowering businesses to monitor their finances closely and make informed decisions.

SAVINGS ACCOUNT

Unlike a current account, a savings account is meant for individuals and encourages them to save money. Savings accounts offer a relatively higher interest rate compared to current accounts, allowing individuals to earn interest on their deposits. These accounts are suitable for personal banking needs, such as saving for emergencies, future expenses, or specific financial goals.

Savings accounts provide a convenient way to deposit and withdraw money through various channels, including ATMs, online banking, and branch visits. This accessibility ensures that individuals can access their funds whenever needed. Additionally, savings accounts offer an opportunity for individuals to grow their wealth. Through the compounding effect of interest, savings accounts enable customers to earn additional income on their deposits. This feature makes savings accounts an attractive option for those who want to save money while earning a modest return on their investment.

CASA RATIO

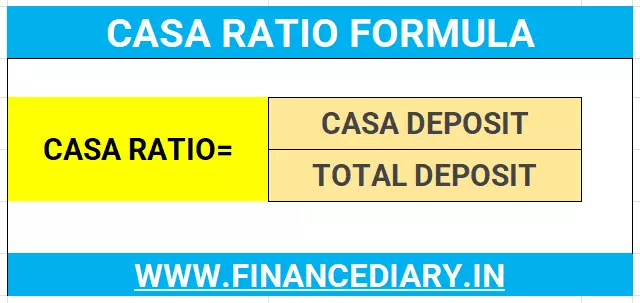

The CASA ratio is an essential metric for banks and financial institutions. It represents the proportion of a bank’s deposits held in the form of current and savings accounts. A higher CASA ratio indicates a healthier deposit base for a bank, as it signifies a larger portion of stable and low-cost funds. Low-cost deposits play a crucial role in a bank’s profitability, as they require less interest expense compared to high-cost sources of funds like fixed deposits or borrowing from other financial institutions. Therefore, banks strive to increase their CASA ratio to improve their operational efficiency and overall financial performance.

CALCULATING CASA RATIO

The CASA ratio is an important metric in banking that helps assess the composition of a bank’s deposit base. It is calculated by dividing CASA deposits by the total deposits of the bank. CASA deposits comprise the sum of deposits in savings accounts and current accounts.

To calculate the CASA ratio, follow these steps:

Step 1:

Determine the deposits in the savings account and current account.

For example, let’s consider XYZ bank with Rs. 10,000 Crores in savings accounts and Rs. 5,000 Crores in current accounts.

Step 2:

Add the deposits in the savings account and current account to obtain the CASA deposits.

In this case,

CASA Deposits = Rs. 10,000 Crores + Rs. 5,000 Crores

=Rs. 15,000 Crores.

Step 3:

Determine the total deposits of the bank. Let’s assume the total deposits are Rs. 35,000 Crores.

Step 4:

Divide the CASA deposits by the total deposits to calculate the CASA ratio. Using the above figures,

CASA Ratio = Rs. 15,000 Crores / Rs. 35,000 Crores = 42.85%

INTERPRETING THE CASA RATIO

In this example, the CASA ratio of 42.85% indicates that 42.85% of the bank’s deposits are utilized for transactions, while the remaining 57.15 % are long-term deposits that the bank can use for lending purposes.

Understanding the CASA ratio helps banks assess the stability and cost of their deposit base. Higher CASA ratios are desirable as they indicate a larger proportion of low-cost and stable funds, reducing a bank’s reliance on expensive sources of funds. This, in turn, improves the bank’s profitability and liquidity position.

By regularly calculating and monitoring the CASA ratio, banks can make informed decisions regarding their deposit strategy and overall financial performance.

BENEFITS OF CASA FOR CUSTOMERS

CASA offers numerous benefits for customers, ensuring convenience and security in their banking experience. With both current and savings accounts, customers can easily access their funds and make transactions. Whether it’s paying bills, transferring money to other accounts, or making online purchases, CASA provides the necessary infrastructure for swift and secure financial transactions.

Savings accounts, in particular, provide an avenue for individuals to save money and earn interest on their deposits. The compounding effect of interest allows customers to witness their savings grow over time. Some banks even offer specialized savings accounts with higher interest rates or additional benefits tailored to specific customer segments, such as students, senior citizens, or women. This customization ensures that customers can choose the account that best suits their needs and goals.

BENEFITS OF CASA FOR BANKS

Banks also benefit significantly from CASA. Firstly, the low-cost deposits from current and savings accounts help banks reduce their cost of funds, thereby improving their net interest margin and profitability. By relying on these

stable and low-cost funds, banks can minimize their reliance on high-cost sources of funds, such as fixed deposits or borrowing from other financial institutions.

Secondly, a higher CASA ratio enhances a bank’s liquidity position. The availability of a stable source of funds allows banks to meet customer demands for loans and investments. CASA deposits provide a reliable base that banks can utilize for lending or investment activities, ensuring their liquidity remains intact.

Furthermore, a robust CASA base strengthens a bank’s customer relationships and brand loyalty. Customers tend to maintain long-term associations with banks that offer reliable and convenient banking services. By providing seamless access to funds, offering competitive interest rates, and catering to specific customer segments, banks can enhance customer satisfaction and loyalty.

FAQ’s

1: How is the CASA ratio calculated?

The CASA ratio is calculated by dividing the sum of current account and savings account deposits by the total deposits of a bank.

2. Higher CASA ratio means?

It means banks will get the funds on lower cost.

CONCLUSION

Dear reader in this article you get to know about CASA full form in Banking, about current accounts, about saving bank accounts, CASA Ratio, Benefits of casa for customers, Benefits of casa for banks. In conclusion, CASA, which stands for Current Account and Savings Account, forms the foundation of a bank’s deposit base. Current accounts facilitate frequent transactions for businesses, while savings accounts encourage individuals to save money and earn interest on their deposits. The CASA ratio serves as an important metric for banks, indicating the proportion of low-cost and stable funds in their deposit base. If you have any query regarding this article kindly comment below.